What Does Return Item Chargeback Mean? Easy Merchant’s Guide

Key Takeaways

- A return item chargeback happens when a check or ACH payment bounces.

- The bank reverses the deposit and may charge you a fee.

- It’s not the same as a credit card chargeback.

- Common causes include insufficient funds, closed accounts, or fraud.

- If it happens, you lose the funds and must request another payment.

- It’s usually not reversible.

- To save time and hassle, you can automate chargeback protection.

As an eCommerce merchant, you’re no stranger to financial hiccups—whether it’s chargebacks or the dreaded payment disputes. If you’ve ever seen “return item chargeback” pop up on your bank statement, you probably had a moment of frustration (or maybe even panic).

So, what does a return item chargeback actually mean? And more importantly, how does it impact your business? Let’s break it down in a way that makes sense for merchants using platforms like Shopify, WooCommerce, BigCommerce, and payment processors such as Stripe, PayPal, and Shopify Payments.

This is what’s in store:

What Does Return Item Chargeback Mean?

A return item chargeback happens when a check you deposited into your bank account bounces. This could be due to insufficient funds, a closed account, or another issue with the check writer’s bank. When this happens, the funds that were initially credited to your account get reversed, and your bank may slap you with a fee for the trouble.

Note that return item chargebacks are primarily associated with checks, but it can also occur with ACH payments (electronic bank transfers) and, in rare cases, with certain debit transactions—but not with credit card payments.

This isn’t the same as a credit card chargeback, where a customer disputes a transaction and gets their money back. Instead, a return item chargeback is strictly a banking issue related to bad checks—but it can still cause cash flow problems, especially if you rely on checks for large transactions.

You might also like: Shopify Chargebacks: How to Avoid & Manage Payment Reversals

How it Appears on Your Bank Statement

Different banks use different terms for this issue, but here’s what you might see:

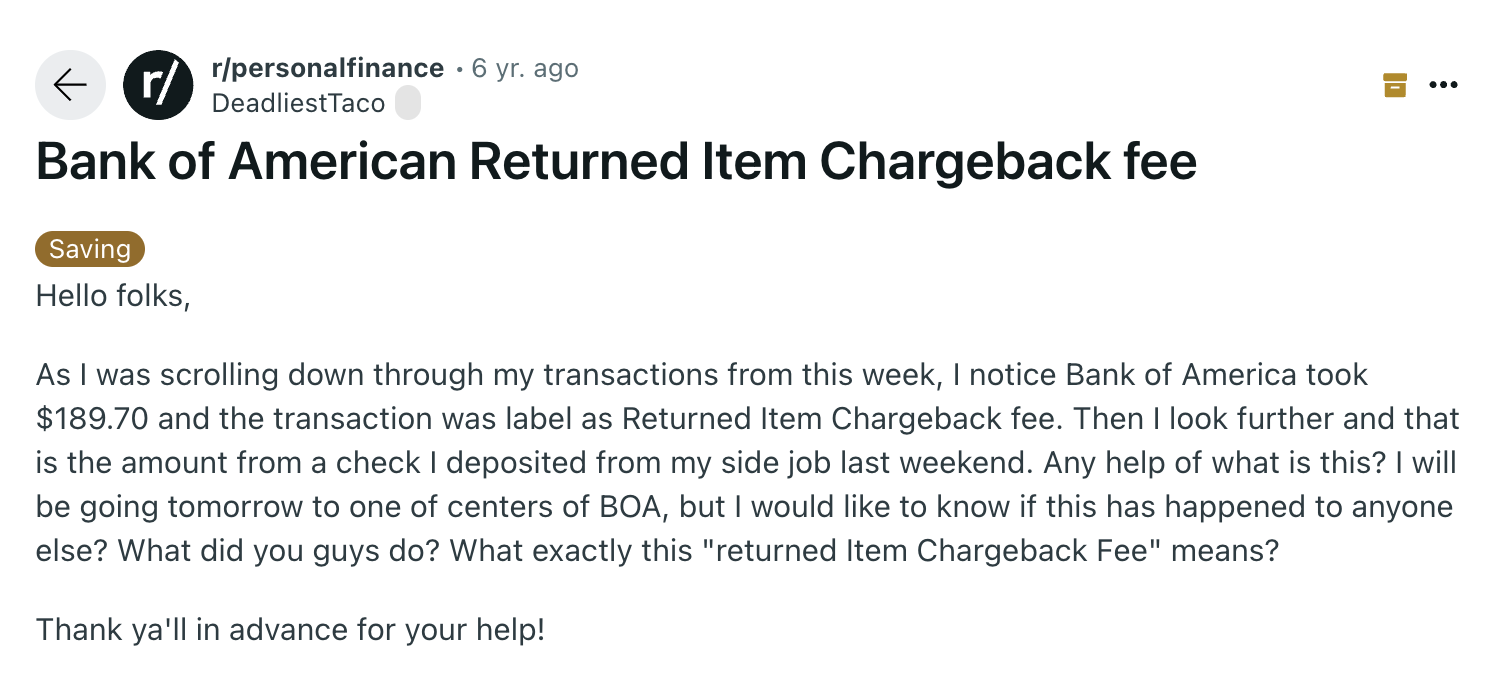

- Bank of America: Return Item Chargeback Fee

- Wells Fargo: Deposited Item Returned

- TD Bank: DEP Return Chargeback

- Chase: Returned Item Fee

Regardless of the name, the outcome is the same: you don’t get the money from the check, and your bank may charge you a fee on top of it.

Does Chargeback Mean Refund?

Not exactly. A chargeback and a refund aren’t the same thing.

Here’s the difference:

- Refund → The merchant willingly gives money back to a customer for a return or dispute.

- Chargeback → A bank forcibly takes money from the merchant due to a dispute.

- Return Item Chargeback → A check gets bounced, and the depositor (you) loses the funds and may get hit with a fee.

If a customer asks for a refund, you’re in control of that process. But if you get hit with a chargeback—whether from a credit card dispute or a bad check—you’re at the mercy of banks and payment processors.

Why Did My Bank Do a Chargeback?

If you received a chargeback from your bank, it’s likely due to one of these reasons:

- Insufficient Funds: The check writer didn’t have enough money to cover the check.

- Closed Account: The account was no longer active when the check was written.

- Stop Payment Order: The person who wrote the check canceled it before you deposited it.

- Fraud or Errors: The check was fake, altered, or contained incorrect information.

This puts you in a tricky spot because you might have already provided the product or service before realizing the payment was worthless.

What Happens if You Accept a Chargeback?

If you accept a chargeback, whether it’s from a bad check or a disputed credit card transaction, you’re agreeing to lose that money—For return item chargebacks, this can be frustrating because you likely accepted the payment in good faith.

Here’s what happens next:

- Your bank removes the deposited amount from your account.

- You might get hit with a return item fee (varies by bank).

- You need to contact the check writer to request another form of payment.

For merchants, this is a huge inconvenience—especially if you’re dealing with multiple checks or high-ticket transactions.

Is a Return Item Chargeback a Bounced Check?

Yes, but with a twist.

A bounced check is what happens on the check writer’s end—their bank rejects the check. A return item chargeback is what happens on your end—your bank takes the funds back and possibly charges you a fee.

Think of it this way:

- Bounced Check → The person writing the check has a problem.

- Return Item Chargeback → You, the person depositing the check, now have a problem too.

Can a Return Item Chargeback Be Reversed?

In most cases, no. Once a check bounces, your bank treats it as a bad payment and won’t redeposit it automatically.

However, there are a few things you can do:

- Contact the check writer or customer → Ask them to send another payment method (preferably not another check).

- Request a bank correction → If you believe the return was a mistake, contact your bank to dispute it.

- Use a check verification service → If you accept checks regularly, services like TeleCheck or Certegy can help reduce risk.

But let’s be honest—accepting checks in 2025 is risky. There are faster, more reliable payment options, and if you run an online store, there’s no reason to be dealing with paper checks in the first place.

How to Avoid Return Item Chargebacks & Protect Your Business

Since return item chargebacks can disrupt your cash flow and cause unnecessary fees, it’s best to prevent them altogether. Here’s how.

1. Switch to Secure Payment Methods

If you’re selling online, ditch paper checks and use:

- Credit cards (with fraud protection)

- Digital wallets (PayPal, Apple Pay, Google Pay)

- Buy Now, Pay Later (BNPL) services (Afterpay, Klarna)

2. Verify Funds Before Accepting Large Checks

For in-person transactions, consider using a check verification service. Some banks also offer real-time balance checks, so you can confirm that a check will clear before accepting it.

3. Use a Chargeback Prevention Tool

Whether you’re dealing with credit card chargebacks or check-related chargebacks, having a solid dispute management system in place is crucial. That’s where chargeback automation comes in.

The Best Way to Manage Chargebacks? Automate It.

If chargebacks are draining your time and money, it’s probably time to automate the process.

Chargeflow offers AI-powered chargeback management, so you don’t have to waste hours disputing chargebacks manually. It integrates with most eCommerce platforms, including Shopify, WooCommerce, Magento, and major payment platforms like Stripe, PayPal, and Square, ensuring you win more disputes with less effort.

👉 Stop Losing Money on Chargebacks—Try Chargeflow Today

Final Thoughts

A return item chargeback is just another way banks make your life harder when a customer’s check bounces. Unlike credit card chargebacks, which involve disputes, a return item chargeback happens when a deposited check gets rejected. While frustrating, you can mitigate it with modern payment solutions and automated chargeback protection.

TL;DR: Stop accepting checks. Use Chargeflow to protect your business. Move on with your life.

Subscribe to the Aurajinn blog to receive updates when we share new content!

Ashley is a freelance copywriter and the founder of Aurajinn. She's been working in eCommerce and technology for over a decade. Here, she shares her best cyst-like gems of wisdom to help new and intermediate online sellers level up their operations.